Rethinking Money: My Path to Financial Stability

How I turned a fiscal nightmare into a realistic future of hope

By Philip Francis Anderson:

Activist and Podcast Host Campaigning for Change

Transforming turmoil into triumph: my inspiring story from financial despair to economic control. I reveal the life-changing secret that could help you too.

Key Takeaways:

- Personal Sacrifice Pays Dividends

- Budgeting is Both an Art and a Science

- Fresh Ingredients and Home Cooking are Financial Lifesavers

- Energy Efficiency is Crucial During a Crisis

- Upgrading Appliances Can Be a Game-Changer

- Practicality and Forward Planning are Your Best Friends

Copyright © 2024. All rights reserved by Philip Francis Anderson. This article is the property of Philip Francis Anderson and is protected under UK copyright law. Unauthorized reproduction, distribution, or use of this text, or any portion thereof, without the expressed written consent of Philip Francis Anderson, is strictly prohibited. For permissions, please email the copyright owner.

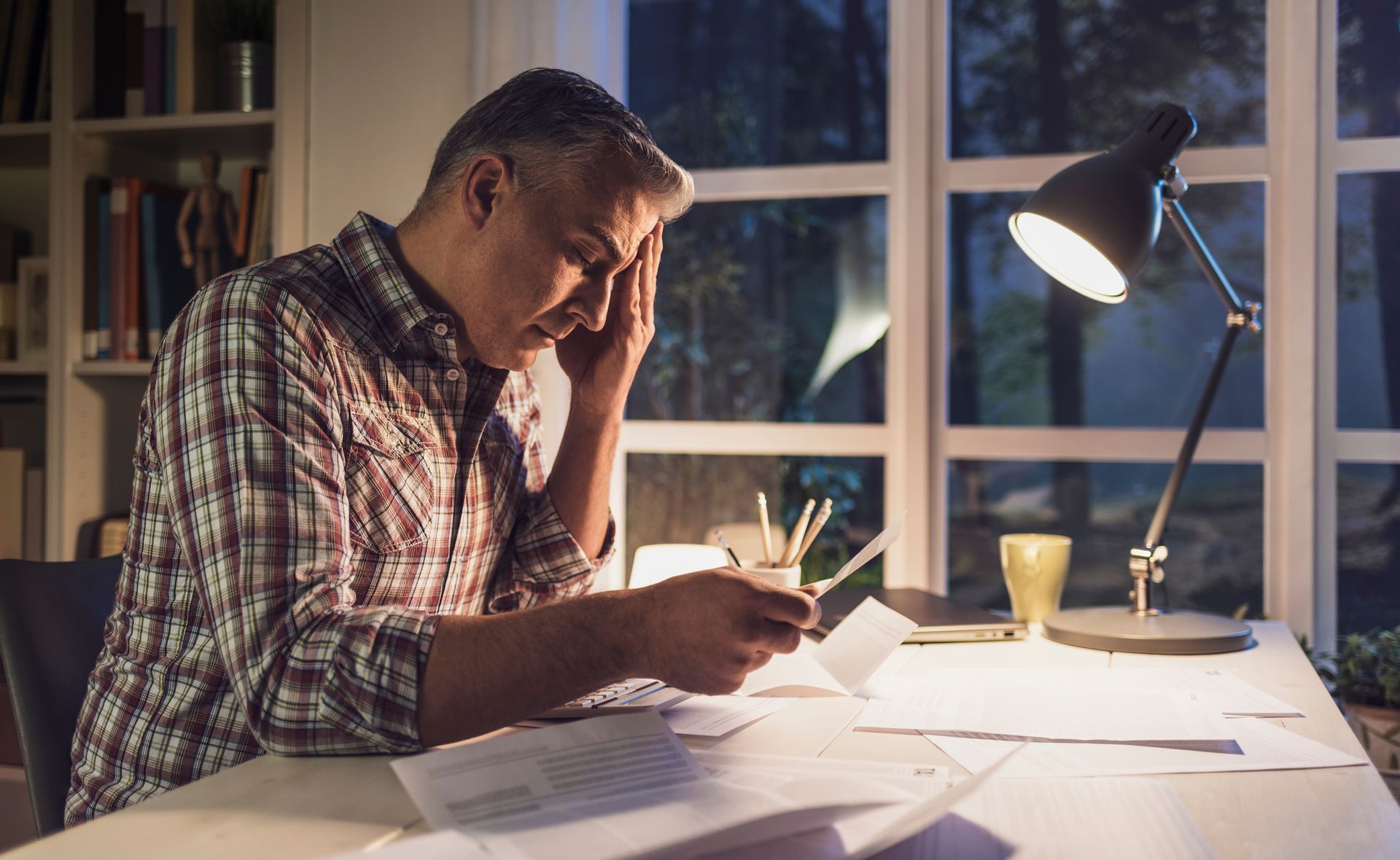

Have you ever felt like your financial troubles were spiralling out of control, leaving you sleepless and anxious? That’s exactly where I found myself—when the pound sign became a symbol of dread and fear blurred the line between sleep and reality. I was caught in a relentless cycle, where money dictated my every move, trapping me in a fog of insomnia and endless worry. But what if I told you there’s a way out—a way to reclaim control and rethink your relationship with money?

For me, this nightmare began after a traumatic divorce, business losses, and the looming threat of losing my son. I used alcohol and tobacco in a futile attempt to escape the crushing anxiety. Each day blended into the next, as fear of failure consumed me, and the burden of financial turmoil deepened.

Money’s dominion stripped away my rational thought, rendering me a mere puppet to its whims. It wasn’t just the numbers that overwhelmed me; it was the feeling of being completely powerless. But there is hope. Join me as I share the hard lessons from my journey out of this dark place and into economic stability. This story is not just about managing money—it’s about reclaiming your life, making tough choices, and finding hope when it seems like all is lost.

What would it mean for you to take back control, not just of your money, but of your peace of mind? Together, let us explore how you can navigate these challenges and emerge stronger, just as I did

Introduction

For a time, it was money controlling me. After my traumatic divorce, business losses, and the possibility of losing my son, I was overwhelmed by stress and anxiety. I spent excessively on unnecessary purchases, leaving me with no surplus funds.

My impulsive decisions led to sleepless nights as I struggled to meet financial obligations, endlessly worrying about my child and how to hold on to him. I was consumed by a growing sense of despair, each new bill adding to the gnawing anxiety that kept me awake at night. In short, I had become financially irresponsible, with nobody to blame but myself.

The turning point came in the autumn of 2010 when I realised that reclaiming control of my money was essential for rebuilding my life and letting go of the past. The previous four years had been sheer torture, struggling to come to terms with an acrimonious break-up that cost me almost everything. Losing my businesses in 2009—and family home three years prior—was manageable, but not my child.

I therefore saw reclaiming my finances as a way of regaining control and finding the much-needed funds to pay for additional legal costs to secure reasonable contact with my son and for urgent household maintenance. It was as if a fog lifted, revealing a clear path out of the chaos. This newfound energy was the saving grace for my relationship with him. Today, we have never been happier.

Have you ever found yourself in a similar situation, feeling overwhelmed by financial burdens while trying to navigate the emotional turmoil of a split? If so, might not taking control of your finances be one way of rebuilding your economic and mental well-being? Here is how I did it.

Rather than letting money rule me, I began diligently tracking my expenses, cutting back on excessive spending and saving a portion of my income each month, using my money to invest in my goals and build an emergency fund. It was about settling for less, not striving for more—a case of prioritising essentials over non-essentials. In so doing, I felt empowered and secure, knowing I could now handle the expected, as well as the unexpected, expenses, like the time my guttering failed, and I needed replacement doors and windows and my decision to study for a BA in Philosophy with the Open University. In this way, money began to work for me once again, helping me achieve my goals and improve my physical and mental wellness without the need for debt.

Actionable Tip:

During a financial crisis, I suggest that you take a step back and assess your situation calmly. Prioritise your essential needs and develop a clear plan to tackle your debts and cut back on discretionary spending. Seek advice from financial counsellors if needed. By staying organised and focused, it is possible for you to regain control and start rebuilding your life.

Being in control of my money means there are no interest charges, no penalties for overdue payments, and no debt collectors knocking at my door. Why? Because it is my own money I am using. And I’m not talking loans and overdrafts. Hence, when I want to reward myself for a job well done, whether it is a meal out with a friend or a short weekend break, the funds are there to cover it.

My experiences exemplify the “terrible master and excellent servant” syndrome, a term used by American showman, businessman and politician Phineas Taylor Barnum to describe money. When money controls a person, it causes anxiety and misery, but when one remains in control of the money, money works to advance their goals without debt and impulsive spending.

Sadly, countless individuals believe they are in control, but their spending habits often tell a different story. As we have seen, I fell victim to money’s mastery after my traumatic divorce in 2006, where money became my “ruler” until I reclaimed control in 2010. This time, though, I made it my ‘excellent servant’ which is how I managed to transform this financial and emotional nightmare into a realistic future of hope.

However, before I could achieve my goal of economic stability, I had to confront a fundamental question: What truly constituted my needs versus my wants? Understanding this distinction was crucial in making the tough decisions that paved the way to financial control.

With this foundation, let’s explore how you can navigate your own financial crossroads and achieve stability without falling into debt, just as I did. As a token of my appreciation, I am offering you a range of resources, including a comforting home-spun recipe that demonstrates how frugality and creativity in the kitchen can positively impact both your health and your finances. These resources are divided into two categories: Actionable Tips and Learn More. You’ll find them within most subsections of this article under their respective headings. Each resource includes links to reputable sites filled with advice, tools, and practical solutions to support your financial journey.

The Difference Between Needs and Wants

The Earth's resources are now strained to sustain the needs and wants of the

human population, which continues to escalate. -

Sharon Gannon.

Have you ever found yourself wondering about the difference between a need and a want? It’s a subtle distinction, but one that can profoundly impact your financial well-being. Needs are essential and less of a drain on your finances, while wants can be money-hungry and pose a threat if not controlled.

Let’s play a little game. Imagine a parent grocery shopping with their child. The child spots some sweets and asks for them, but the parent, mindful of the budget, says no. Conversely, think back to the last time you felt the urge to up your overdraft to buy the latest smartphone, even though your current one works just fine. These common scenarios highlight the crucial difference between needs and wants. Can you see it? Let us explore, shall we.

Needs

Needs are the essentials we must have to survive and function daily. They include food, shelter, clothing, healthcare, and basic utilities. Without these, life becomes challenging, if not impossible.

In our grocery shopping example, the parent knows the family budget must prioritise nutritious food over treats. This small but informed decision ensures the family can cover all necessary expenses. By focusing on needs, the parent shows the importance of allocating resources wisely to maintain stability and well-being.

Actionable Tip:

When you’re considering a purchase, ask yourself if it’s essential for your basic well-being. Is it something you truly cannot live without? If it’s not crucial, it’s likely a want. This simple question can help you save money for life’s true necessities.

Learn More:

For a detailed guide on distinguishing between needs and wants and practical budgeting tips, visit NerdWallet's Needs vs. Wants Guide

Wants

Wants, on the other hand, are the non-essential items or experiences that add pleasure, comfort, or convenience to your life. These are things we desire but can live without, like that morning latté from the café, the latest smartphone, or dining out at fancy restaurants. While enjoyable, these purchases can quickly drain your funds if not kept in check.

I’ve been there myself. From 2006 to 2010, I frequented fancy restaurants, indulged in the demon in the bottle, and smoked tobacco. These non-essential items left me short on funds long before my next paycheck. In my experience, it was these non-essential items that were the culprit, consuming my money and leaving me out of funds before the end of the month.

It’s one of the reasons people turn to interim loans and overdrafts to tide them over. However, these loans and overdrafts all have to be repaid, leaving them even shorter the following month—and so they end up borrowing more, creating a vicious cycle. Eventually, even basic essentials like food and rent become difficult to cover.

Make no mistake, it is easy to blur the lines between needs and wants, especially in a society that often equates success with material possessions. Contributor Ruth Williams is living proof. She shared, "I'm trying at this but not succeeding. I think it's my way of cheering myself up to buy stuff. I always convince myself I'll stop after this last purchase. It's a hard habit or addiction to break." Ruth’s struggle resonates with many of us, highlighting how wants can sometimes take over our better judgement. In fact, according to UKAT,, there are between 200,000 and 350,000 shopping addicts in the UK alone, a habit they believe is akin to that of “drug and alcohol addiction.”

Learn More:

To see how you can balance needs and wants in your budget, check out NatWest’s MoneySense Needs vs. Wants Teaching Resources

For information on impulsive buying, check out: Shopping addiction information & treatment | UKAT

As we transition from understanding wants to the broader implications of our spending habits, let's delve into the moral dilemma of excess and its impact on both our finances and the environment.

The Moral Dilemma of Excess

Imagine yourself walking through a bustling high street, with the latest gadgets and fashion items displayed enticingly in shop windows. Do you find yourself drawn to the glitz and glitter on offer? Do you feel an urge to reach for your credit card or cash, enticed by the thought of owning something new and shiny?

A report by Empower.com showed that 29% of Americans felt they spent too much on personal comforts, while 6% thought they didn’t spend enough on guilty pleasures. Conversely, in the UK, a survey by the Office for National Statistics revealed that 30% of residents believe they overspend on non-essential items, while 7% feel they don't indulge enough. This shows a common struggle with balancing personal comfort and financial prudence.

As we have seen, it's easy to be swayed by the allure of luxuries, making purchases that offer temporary satisfaction but lead to long-term financial strain. I think we are all guilty of buying something on impulse, only to regret it later when bills come due. These choices not only impact personal finances but also contribute to environmental degradation through increased waste and resource consumption.

Sharon Gannon, whom I quoted at the start, warns of the environmental implications of excess, claiming people take more than they need or want from the earth. For instance, the excessive consumption of fast fashion leads to massive amounts of clothing waste and pollution. According to the Plastic Pollution Coalition, nearly 70 billion items of clothing produced each year are made of plastic, releasing at least 1.4 quintillion plastic microfibres into the ocean, compounded by social media platforms like Whatsapp, Tiktoc and X. Commenting on this, Open Access Government says: “The most environmentally-harmful but acceptable trend of the internet is fashion ‘hauls’ – where people bulk-buy clothing to gain more followers, and consequently, consumers. Often, these hauls are sponsored by the companies fuelling this problem.

What is ‘trendy’ one day, may be completely eroded the next.” This behaviour reflects a deeper moral and ethical issue of overconsumption and exploitation of resources.

Actionable Tip:

Before making an impulse purchase, pause and imagine a future where our planet suffers severe climate change—scorched landscapes, polluted oceans, and unbreathable air. Ask yourself if the item is truly necessary. Restraining your wants saves money, reduces your carbon footprint, while forcing manufacturers into producing less. Your mindful choices today can help prevent this bleak future and create a healthier planet for tomorrow.

Understanding the difference between needs and wants is the first step towards financial balance. By prioritising your essential needs and making informed decisions about your wants, you can achieve greater financial stability and peace of mind.

Balancing Needs and Wants

How do you make financial decisions? Consider the difference between buying groceries for the week and splurging on an expensive dinner out. What drives these choices? Is it a desire for immediate gratification, social pressure, or perhaps a way to reward yourself after a long week? Are you motivated by practicality and necessity, or do emotional factors play a significant role? When you distinguish between your needs and wants, you gain a fresh outlook on your spending habits, enabling you to make more informed and balanced financial decisions.

In reflecting on my own experiences, I often found myself buying things impulsively. How did it make me feel in the moment? Excited, perhaps, but that feeling quickly faded when I reviewed my bank statement later. My experience taught me that by prioritising essential needs like food, shelter, and healthcare, I could secure my basic well-being. This meant focusing on paying rent or mortgage and buying nutritious groceries, before considering any luxuries. To reach that point, required copious self-discipline and determination; something we will explore in the section: A Financial Revelation. Conversely, think about the non-essential items you frequently buy. How often do these purchases bring lasting satisfaction? What if, instead, you invested that money for say an emergency fund or a planned family holiday, for example? Consider how much peace of mind that could bring.

Actionable Tip:

Implement the 24-hour rule for non-essential purchases. According to a report published in Chase UK, delaying a purchase by just one day can significantly reduce the likelihood of impulse buying. By waiting 24 hours, you allow yourself time to evaluate whether the purchase is necessary, often finding that the initial impulse fades, leading to more rational decision-making. I learned this the hard way, but it was a game-changer.

Moreover, achieving this balance helps us see the bigger picture—our long-term financial health and goals. By being more mindful of our spending, we can avoid the pitfalls of instant gratification and focus on what truly matters. Think about how your spending aligns with your values and goals. In my journey, as you will learn in A Financial Revelation, it was about exercising self-discipline.

Evidence shows the importance of this approach. According to a study by the Federal Reserve Board, nearly 40% of Americans couldn’t cover a $400 emergency expense without borrowing or selling something. This highlights the need for an emergency fund. Cutting back on wants could help you build this safety net.

In reflecting on Ruth's story earlier on in this section, we see how challenging it can be to curb impulsive spending and find financial balance. Her struggle reminds us that finding harmony is a journey, not a destination. Ask yourself: What steps can you take today to move towards a healthier financial balance? By reassessing your priorities and making deliberate choices, you can uncover a surprising path to economic freedom.

As you start to find that balance between needs and wants, it's important to understand that knowledge alone isn't enough. True financial wisdom involves applying that knowledge wisely in various situations. This brings us to an interesting analogy involving a cowboy and his horse...

From Knowledge to Wisdom

There is an old cowboy saying about what you need: “If it doesn’t fit on your horse, you don’t need it.” This saying emphasizes the importance of prioritizing essentials, suggesting that only the most critical items should be carried. While it’s a great reminder to focus on what’s truly necessary, it doesn't fully capture the complexity of distinguishing between needs and wants in our modern lives.

The saying assumes people know in advance what a need is. Historically, needs have always been the essentials for survival—things like water, food, and shelter. However, while the specific items might have evolved over time, the principle remains the same: needs must be life-essential. But in today's world, determining what is truly essential can be more complex, especially when considering personal and professional needs.

Take Gavin’s perspective. Gavin is the founder and creator of the award-winning customer services app, WelcoME. He shared, "I am a living, breathing example of someone who lives with everything he needs. Embracing this has been my greatest moment of awareness. I have nothing and have never been happier." Gavin sold his house for a motorhome to pursue his business, saying, "In my motorhome, I have an iPad, an iPhone, and 250 GB of anytime data." For Gavin, these tools are essential for his work, even though they are not traditional life-sustaining items like food and shelter.

This raises an interesting question: Are there various categories of need? In addition to our life’s essentials of food and shelter—which are non-negotiable for survival—there are things people might need to do their jobs, such as Gavin’s iPad and iPhone. These items, while not essential for survival, are crucial for his work and therefore become necessary in this context. So, how do you decide what is important in this situation?

Actionable Tip:

Allocate funds for rent and groceries before considering upgrades to your work equipment. It’s a balancing act because you need tools to work, which is what affords you the income for life's essentials. To get this balance right, prioritize your essential needs in line with your budget first, then assess what’s left for non-life-threatening needs. This approach helps you maintain financial stability and focus on what truly matters.

In analysing the cowboy's saying further, it becomes clear that simply knowing the difference between needs and wants is insufficient. For instance, a rider might reason, “I’d carry the phone in my pocket,” but if it takes up space that could be used for a food pouch, they could find themselves in trouble if their horse fell ill in the middle of nowhere. Without a mobile signal to raise the alarm and running out of food, they might be stranded. That extra food pouch could sustain them for several days, by which time their horse might recover, enabling them to continue their journey or seek help.

According to the Stanford Encyclopaedia of Philosophy, you can have knowledge and no wisdom, but you cannot have wisdom without knowledge. It takes wisdom to make the judgment suit the circumstance. Gavin's response further illustrates this point: “The cowboy who puts wants on their horse instead of needs soon finds out that they are putting their life at risk or making it very uncomfortable.” This ‘act-now-regret-in-leisure’ approach, first expressed in print by William Congreve, highlights the difference between having knowledge of what is essential and applying that understanding wisely. It’s a case of cutting your cloth according to your means and exercising good judgment.

Learn More:

From Survive to Thrive: 5 Levels of Human Needs

Living Within Your Means

Live within your income by avoiding loans to fuel a habit. – Philip F Anderson.

Understanding the difference between needs and wants is also about acceptance. If you are to stand a chance of making any progress, accepting the raw reality of your financial circumstances—however painful—is a crucial step toward taking back control. But what does that mean?

Here, the raw reality means recognising the actual money you have, rather than the money you believe you ought to have and learning to cut your cloth according to your means.

This means not exceeding your prescribed income. If your earnings a month are £1,000, then trying to spend £2,000 with the help of loans and overdrafts is simply not feasible.

The concept of cutting your coat according to your cloth emphasises the need to align your lifestyle with your financial reality. This may involve making tough choices like forgoing luxuries, such as holidays or a car, and opting for a more sustainable living arrangement. By doing so, you can steer clear of the pitfalls of debt and maintain financial stability.

Relying on loans to fund excessive spending only deepens financial difficulties. High-interest rates on personal loans and credit cards can quickly escalate, trapping you in a cycle of debt. Instead, prioritise what you can realistically afford within your current income. This may involve setting a firm budget, seeking out discounts, or opting for free or low-cost activities.

This method promotes lasting financial security and a sense of control, allowing you to secure your future without the constant pressure of debt.

A report by the Office for National Statistics (ONS) revealed that households who live within their means experience less financial stress and greater overall well-being. By aligning your spending with your income, you can achieve a sense of control and security, knowing that you are not overextending yourself financially.

Ultimately, living within your means is about making deliberate, sometimes challenging decisions to stay within your financial boundaries. It's not about yearning for more, but about optimising what you already have. This approach not only fosters better financial management but also brings peace of mind and long-term stability.

Actionable Tip:

When you feel envy, focus on your own progress and ambitions. Remember, comparing yourself to others can lead to unnecessary spending. Be grateful for what you have, and remind yourself of the benefits of financial stability as excessive spending on impulsive purchases is the slippery slope to economic ruin.

Learn More:

Paul Lewis’ Money Box: Your Toolkit for Balancing Your Budget, is an excellent resource.

So, just to recap, understanding the difference between needs and wants is essential for achieving financial stability. Needs are the basics required for daily living, such as food, shelter, and healthcare. Prioritising these ensures we can maintain our well-being. Wants, however, are non-essential items that add pleasure and comfort but can strain finances if not managed wisely. By focusing on our needs and limiting spending on wants, we can save money and avoid financial stress. This balance helps us make informed decisions, ensuring we allocate resources efficiently and maintain financial health.

Useful Resources

For further insights into managing your finances by distinguishing between needs and wants, explore these resources:

- NerdWallet's Needs vs. Wants Guide: This guide provides a comprehensive look at how to budget effectively by understanding your needs and wants.

- Consumer Credit’s Needs vs. Wants Infographic: This infographic offers a visual breakdown of needs versus wants and practical tips for managing your budget.

- NatWest’s MoneySense Needs vs. Wants Teaching Resources: This resource provides educational materials on needs vs. wants, useful for both adults and children.

It was this acceptance of the raw realities of my own financial circumstances that played a crucial role in my journey to economic solidity. By reassessing my priorities and making deliberate choices, I uncovered a surprising path to freedom.

A Financial Revelation

The most difficult thing is the decision to act, the rest is merely tenacity. -

Amelia Earhart.

Never a true word spoken. In 2010, my life felt like a chaotic whirlwind. My home, a basic yet demanding 1885 Victorian terraced, was crying out for serious maintenance—projects that seemed financially out of reach. Endless reminders of what it was like to live in a century-old property, were a regular occurrence and became a huge drain on my physical and mental health. Add to that, a recent divorce that left me emotionally and financially drained; My nerves were a quivering wreck. I was living alone, reeling from the loss of two businesses and struggling to regain a semblance of stability.

Prior to this, my income was almost double with few financial worries. I had the means to educate my son at a decent preparatory school and enough to support our modest life-style. My matrimonial home was a four-bed semi conversion with ample gardens and lawn to the rear, a property my wife and I had bought three years prior to us getting divorced into which I had invested thousands on various modifications. Therefore, you could say, life was good. I always knew things were not what you would call plain sailing between us, but I did not envision I’d be homeless three years on after nine years of marriage.

Yet, divorce I did, where my income practically halved under £40,000 per annum, drawn from investments; with each pound spoken for. To make matters worse, I had developed costly habits like heavy smoking and drinking, which, at the time, felt like necessary crutches to get through the day.

As these demands for home repairs grew louder, I realised that ignoring the issues or seeking external financial aid was not a viable long-term solution. Loans were out of the question, as the interest on short to medium-term borrowing would only add to my stress and financial burden. Anyway, my pride would not let me rely on external help —I believed in managing my own financial affairs, no matter how dire the situation. Something had to give. I knew I had to take control, but the path forward was not clear. This realisation marked the beginning of my journey to financial clarity. It was time to face the reality of my situation and find a way to move forward.

Actionable Tip:

Have the courage to face your problems head-on rather than burying your head in the sand. Keep an open mind and be mindful of cognitive biases that can often cloud your judgment. By confronting issues directly and objectively, you can develop realistic and effective solutions to your financial challenges.

The Turning Point

During a particularly sleepless night, lying in the darkness with rain spraying my window, an epiphany hit me. I had to scrutinise my finances down to the last penny. I needed to unearth funds buried in my everyday expenses—something I would have done without a second thought before. I knew it wasn’t going to be easy. When is facing a bitter truth ever easy, especially one created by your own actions? The shame and humiliation of my excess spending had me reaching for my bedside table and my trusty smokes. Tossing back the quilt, I staggered out of bed and over to the open window, lighting my cigarette on the way. My mind was in turmoil.

Somehow, whether it was the nicotine, the spray from the rain blowing in from outside, or both, something clicked in my mind. The huge weight which had been weighing down on me, lifted. At that precise moment, I made a pact with myself to get down to it first thing in the morning.

Actionable Tip:

To know you are truly in control of your finances, ask yourself if money is serving your goals rather than dictating your actions. Remember the words of Phineas Taylor Barnum from the outset of this article: money is a "bad master, but a good servant." When you make conscious spending decisions and save strategically, such as investing in education or saving for a home, you are making money work for you as a good servant. Conversely, if you find yourself constantly worrying about debt or making impulsive purchases to impress others, money is acting as a bad master, dictating your actions.

Tough Decisions

True to my word, and countless mugs of fresh coffee later, I got down to it.

The first step was facing the hard numbers. I began by prioritising the legal fees and maintenance tasks and estimating their costs. I wrote them down in order of urgency. Addressing structural issues threatening my home's foundation was my second pressing need. Number one was finding the funds to service the additional legal costs for child contact estimated at £7000. Where would the money come from?

Part of the answer, to my surprise, lay in confronting one of my most expensive habit: smoking—caressing the half empty packet of B&H Gold on my desk.

I was spending a staggering £3,000 annually on cigarettes. This was 2010 when 20 B&H were anywhere between £6.90 and £7.20. Today, they are one and a half times that at £17.95. Quitting seemed like madness at a time when my stress levels were through the roof, but I realised it was a necessary sacrifice. So quit I did—after I had smoked the remainder of that last packet; all bar one. Do you know, I held on to that old fag box and its solitary smoke for the biggest part of thirteen and a half years. I thought that by holding onto it, I would have to work twice as hard to resist the burgeoning desire. Silly as it may seem, my method worked.

That is not to say I was not tempted. Oh yes; especially when alcohol was involved. But I digress. Back to my quitting days. It happened and I could scarcely believe it.

I therefore started transferring £57.69 weekly into a savings account—the same amount I would have spent on cigarettes. It was a painful and slow process, battling cravings and facing the void left by my habit, but each week, as I watched the savings grow and my fingernails shrink, it fuelled my determination. It was thrilling and excruciating. Seeing my savings account balance rise gave me a much-needed sense of accomplishment and control.

Scrutinising my finances further, I discovered additional areas where I could cut costs. These changes, while requiring personal sacrifice, had a surprisingly positive impact on my financial stability and emotional wellbeing. Here is what I did:

Cutting Costs Elsewhere

Also high on my list for the chop was fine dining. I stopped my regular restaurant visits, reserving them only for special occasions. As with smoking, This too saved me £3,000 annually. I could not believe it. I was now £6,000 better off just through cutting out smoking and lavish meals out. Five hundred smackers extra in the bank every month; six whole grand over 12. The beauty of it was, it was my money; money I had had all along if I had only realised it.

Actionable Tip:

Reflect on your own spending habits. Identify one costly habit you can cut back on or eliminate entirely. Redirect the savings towards an urgent financial goal or a savings account.

Learn More:

Part of my problem was living in denial, as though my divorce had never happened, that I was still earning £80,000 a year and could afford everything as before. Yet, the reality was, I could not. I was divorced living in a much smaller house than I was used to, on half my salary and desperately trying to make sense of it all. But make sense of it I did and, once I had started scrutinising my spending habits, realised there were other areas for personal gain.

By switching broadband and landline providers, I halved my bills, saving £50 per month. Staying connected is crucial. However, why pay more for something when you can have more of the same for less?

Skipping weekly coffee shop visits saved £1,040 a year. Admitted, each missed visit felt like a blow to my routine, as those café moments had become small havens of respite. Still, I invested my time into dawn walks, immersing myself in nature, which was far healthier and more rejuvenating; the tearoom now reserved for special occasions.

Cancelling local milk deliveries and switching to supermarket purchases freed up £64 per month. Although I support local services, practicality had to take precedence in my situation.

I must admit, there were moments when denying myself these luxuries seemed like I was piling on the unhappiness—after all, meals out had become my escape, a slice of normalcy in the turmoil. Even so, I clung to my resolve, reminding myself my goal of holding on to my son and rebuilding my life was worth more than temporary comfort. Moreover, cooking at home became both a financial necessity and a therapeutic activity. It encouraged me to host dinner parties, enriching my social life and allowing me to rediscover my love for cooking.

Actionable Tip:

Cooking at home offers numerous benefits beyond just saving money. From a practical standpoint, it allows you to control ingredients and portions, leading to healthier meals. Socially, cooking together can strengthen relationships, creating shared experiences with family or friends. Environmentally, home-cooked meals generate less waste, as you can minimise single-use items and make better use of leftovers. Plus, by choosing locally sourced ingredients, you can reduce your carbon footprint, contributing to a more sustainable lifestyle.

Learn More:

For more details, check out this article on Why Cooking at Home is Beneficial.

Through these efforts, I unlocked annual savings of £7,640, enough to cover all my urgent home maintenance jobs. It also meant I could withdraw £7,000 from my investment fund for the legal fees needed for child contact regarding my son. I could easily replace this amount within twelve months using the savings from my household budget once the maintenance was completed. Phew! I had done it.

Easy to say, though it was anything but at the time—reaffirming Amelia Earhart’s sagacious maxim that “the most difficult thing is the decision to act.” However, ‘to the victor the spoils’ as the age-old saying goes. It was now my task to see it through.

Seeing It Through

Given my mindset then, I could have easily rested on my laurels, basking in what was quite a feat. It was at times like these I would celebrate with a cigarette. I can’t say I wasn’t tempted. The thought of ‘just one to mark this super-duper milestone’ showed the systematic volatility within me; my irrational mind was obviously oblivious to the implications such an action could lead to—a recipe for disaster, indeed. From my older self to my younger self: “Now-now. Don’t be foolish. Do you want to see £3,000 vanish in a puff of smoke?” That is what I find myself still saying today during those rare – and I mean rare – occasions whenever the thought of a ‘quicky,’ as I used to call a smoke, crosses my mind. However, I did not succumb and have been smoke-free for over 14 years.

Within three months of quitting, I had amassed quite a hefty sum. With everything combined, it amounted to a staggering £1,977; enough to cover my damp course and decorating for my dining room.

What did it for me, was watching that initial job in action. It was nothing short of exhilarating. Even booking the maintenance guys for the respective tasks and picking up discounted decorating essentials from my local DIY, gave me enormous pleasure. And to think, that it happened because this one here had made it happen. Although, I feel ‘made’ here in this context, is more than a tad tenuous. I had moved heaven and hell just to reach that initial milestone.

This newfound financial buffer I had unlocked, over time not only provided peace of mind, but it allowed me to address the urgent home maintenance projects and plan with confidence in a far greater way than I had first hoped. More than that, it set me on the path to financial control and stability once more.

To summarise, recognising the need for financial control was pivotal in transforming my life. Faced with a deteriorating home and post-divorce financial strain, I realised external loans were not a sustainable solution. Instead, confronting the reality of my situation and prioritising essential expenses allowed me to find clarity. This journey required significant personal sacrifices, such as quitting smoking and reducing non-essential spending, which translated into substantial savings. These deliberate, informed decisions enabled me to manage my resources effectively, rebuild my life, and ultimately secure a happy and stable future for both myself and my son.

Yet, in the back of my mind, I realised that amid all these tough decisions was a familiar figure, someone who, despite our tenuous relationship, had been instrumental in my own frugality. My father. The discipline and stringency and his meticulous approach to money management I had observed in him growing up, had unwittingly laid the groundwork for my own financial resilience. Despite everything, his influence was unintentional yet profound. The principles he lived by—scrutiny, discipline, and frugality—became the bedrock of my own financial journey. In view of this, let me delve deeper into how his habits, even in our distant relationship, shaped my understanding of money and its management.

Why Knowing Matters in Financial Choices

Annual income twenty pounds, annual expenditure nineteen nineteen and six, result happiness.

Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.

Charles Dickens, David Copperfield.

Education and upbringing play a crucial role in how we manage money. Understanding the difference between Needs and Wants is foundational, but applying that knowledge with wisdom truly shapes our financial behaviour.

Consider two individuals, Emma and John. Emma grew up in a household where financial discussions were open and she was taught the importance of budgeting and saving from a young age. She learned to track expenses, set financial goals, and value delayed gratification. As a result, Emma approaches money with a clear understanding of her goals and the discipline to achieve them. She avoids unnecessary debt and saves diligently for her future.

Conversely, John's upbringing was different. In his household, money was a taboo subject and financial decisions were made impulsively. As a result, John never learned the importance of budgeting or saving. Consequently, he constantly struggles with debt, makes poor financial choices, and feels overwhelmed. He often resorts to payday loans and

credit cards to cover basic expenses, worsening his financial stress.

Emma and John's experiences show that knowing how to manage money is important, but it's the application of that knowledge that truly makes a difference.

As featured above, Charles Dickens aptly captured the essence of financial balance and its impact on happiness and misery. His words underscore the critical balance between income and expenditure, highlighting the consequences of living beyond one's means.

This testament to how education and upbringing shape one's approach to money leads to my own experience.

Look After The Pennies

Growing up, I absorbed money management skills by osmosis, thanks to my father’s meticulous habits. His approach to every penny—right down to the half pennies—yes, I am old enough to remember these—was a constant lesson in financial discipline. He would dole out our pocket money with precision—down to the last ha’penny. His exacting nature extended to my mother. It was a time when men controlled the purse strings. If my mother’s hair bill came to £5.00, he would leave the exact amount—all in ten pences—on the dining table before leaving in the morning, with strict instructions to return any change to the same spot. We boys, knowing there wouldn’t be any, would retort, “What, even out of halfpence?”

This delusional idea of my father’s—that working with money in minor denominations would somehow boost its value—became a source of endless fascination for me. Compared to a five-pound note, a pouch packed with fifty ten-pence pieces gave the appearance of better value, filling one with a deeper appreciation and respect for each coin. While it is true that one might be reluctant to break into a five-pound note for a twenty-pence purchase, parting with two ten-pences from your pouch of fifty coins is far less daunting. Small change was my father’s everyday working capital, with notes reserved for major purchases and holding on to. All his money management took place in private.

The King is in His Counting House

Saturday afternoons were particularly revealing; my father would return from his club, dash upstairs without so much as a 'hello' and lock himself in his bedroom. With my ear pressed secretly against the door, I listened as he meticulously sorted his coins into precise piles before transferring them into his cash box. He kept this miser's steel contraption in his double-doored oak wardrobe, which he kept always locked. It was a source of endless fascination for me, leading me to christen it “The Bank of England.”

That cash box is still in the family as far as I am aware. It first came into my possession on my father’s passing in 1991. Then, when my son was five in 2003, I passed it onto him; and thus began his own journey of sound money management. Now at 26, he is MD of his own company and has been financially independent since the age of sixteen.

Actionable Tip:

Develop a family tradition of money management by teaching your children the importance of saving from an early age. Simple rituals, like sorting coins or maintaining a savings box, can spark their interest and lay the foundation for lifelong financial responsibility. Encourage imaginative play, such as "Let's Pretend" games, to shape their mindset for money management. My son would pretend his teddies were consumers, using my father's inherited cash box as his shop till.

These rituals of my own father intrigued me and sparked my early interest in money management, just as my money habits have inspired my own son.

Early Lessons in Banking

My father’s exactness did not end with his private coin-sorting ceremonies. He often took me along on trips to the bank to pay household bills and inadvertently introducing me to the world of finance at an early age. This early exposure to the practicalities of handling money led to my father opening my first savings account with the Woolwich Building Society just after my sixth birthday.

Nevertheless, my father’s frugality wasn’t just about saving; it was about understanding how small savings could accumulate into substantial funds over time. I would listen to him talking about saving up for various projects, like the time he wanted to install a customised bedroom suite. It was a task which involved meticulous planning and budgeting—something he was quite happy for me to be involved. I remember being with him in his bedroom sitting across from the Bank of England, the plans spread out before him. Just as I had thought, He had worked everything out down to the last penny, with materials prioritised into their own special columns complete with costs.

He then went on to describe his timeline for the job. However, I shall spare you the detail. Sufficed to say, he knew precisely what to buy and when. It was quite exciting hearing him waxing about it all and imagining him ticking things off as deliveries arrived, inspected, and signed for.

Actionable Tip:

Make a habit of reviewing your finances regularly. Schedule a monthly financial check-up to go over your budget, track your expenses, and adjust as needed. Consider involving your children in simple financial tasks, such as budgeting for groceries or saving pocket money, to instil good money habits from a young age.

This principle became a cornerstone of my financial philosophy and influenced my future strategies. Suffice to say, by the time I was thirteen, I had set a wallet target to save up to £100 in one-pound notes and likewise in ten pence pieces for my cash box back home, achieving this with determination and beyond. I had furtively encountered my father’s personal wallet and was amazed at just how fat it was. It was that which gave me the idea. It made my measly target seem like chicken feed by comparison. Even so, It did not deter me.

In fact, This modest sum by today's standards gave me a sense of financial worth and pride. I vowed not to use this fund, keeping it separate from my working capital housed in a different partition of my wallet. Having a ton plus neatly secluded about my person wherever I went gave me a smug sense of satisfaction and did wonders for my confidence and self-esteem.

I realise that I owe much of my financial independence and sound money management to the home-spun wisdom and mercenary approach of my father from where my own no-nonsense attitude to money first originated.

Actionable Tip:

Start a small savings challenge. Set aside a specific amount each week and gradually increase it. Track your progress and celebrate milestones to stay motivated.

Painful Lessons in Sound Money Management

From childhood, I saved and managed my pocket money meticulously, depositing funds from my piggy bank into my Woolwich savings account. My pocket money covered all the usual things: sweets and the like when little, to personal expenses from records to casual clothes when a teenager. My father had always taught me never to ask for more, but to ‘put up and shut up.’ In other words, if you haven’t got it, go without till you do. ‘Neither a lender nor a borrower’ shall be, that was my father. Another of his sagacious maxims was: ‘Don’t ever complain about the food on the table unless you’ve bought it.’

When old enough to walk out with a girl, I would not dream of asking him for an advance on my allowance so I could treat the love of my life to a special night out. The thought of it would have me sweating. Oh no. ‘You’ll just have to tell her she’ll have to wait. The best things come to those who do; it usually does.’

As a teenager, I continued this discipline. I turned pupils’ unwanted items into quick bucks and eagerly took on paid jobs from staff, like emptying classroom bins for £2 a month, with my then commerce Master humorously dubbing me the “bearer of thousands of pounds” who squeaked when he walked. At the end of each term, I would set aside a portion of my surplus for my child’s National Savings account, managed by the school's senior admin clerk.

These early experiences laid a solid foundation for future economic management. It will doubtless come as no surprise to you to learn, that my first job as a junior clerk at the National Westminster Bank and a subsequent crash course in business management led to winning the Shell Livewire business award in 1989. This propelled me into a successful career, and by age 30, I was managing director of two thriving companies: Braille Transcription UK Ltd and Access Global Ltd.

In essence, my father’s meticulous approach to money management profoundly shaped my financial outlook in three key ways. First, his practice of looking after every penny taught me the importance of small savings, demonstrating how they accumulate into substantial funds over time. Second, accompanying him on trips to the bank and opening my first savings account ingrained in me the value of planning and the practicalities of handling money. Third, his detailed budgeting for household projects, like his customised bedroom suite, highlighted the importance of prioritising expenses. These lessons from my father laid the foundation for my disciplined financial habits, enabling me to achieve stability and instil the same values in my son.

This discipline naturally extended into other areas of my life, including my approach to food; another of my pet subjects. Is it one of yours? Science for the senses as I like to call it. Here, let’s explore how choosing fresh ingredients over processed ones proved both healthier and more cost-effective.

Actionable Tip:

Encourage your children to save from an early age by giving them a piggy bank and matching their savings contributions. This not only teaches them the value of money but also fosters financial independence. Over time, they will learn to manage their own funds and make informed financial decisions, which can benefit them throughout their lives.

Fresh vs. Processed Meals: The Real Cost

Cooking is like love. It should be entered into with abandon or not at all. - Harriet Van Horne

Growing up in a boarding school nestled between a beef farm and a market garden, I developed a strong appreciation for fresh ingredients. Cooking with fresh produce was not just a culinary preference; it became a practical and economical choice deeply ingrained in me. I quickly warmed to what was then called Domestic Science, eagerly rolling up my sleeves and donning a PVC apron. Participating in cooking classes and winning the cookery category in the school's Eisteddfod in 1985 and 1986 further fuelled my passion. Yet, becoming a chef was never my ambition. However, it’s one of those necessary activities which I enjoy with a passion.

One particularly formative experience was our weekly supper nights. A group of senior boys and I would each contribute 50p to create one of our favourite house dishes. Each week, a different member chose the dish, and we would all pitch in to prepare it. This tradition taught us to plan, budget, shop, and cook as a team, turning modest contributions into rich, enjoyable meals.

This background made me keenly aware of the cost-effectiveness of cooking at home. Why pay £20 for one takeaway curry when you can make a fresh one at home for £3?

To illustrate how fresh ingredients provide better value and nutrition compared to processed or takeaway options, here is a practical comparison that brings this to life. Each ingredient tells a story of savings and quality, turning your kitchen into a vibrant marketplace.

Actionable Tip:

Create a weekly menu by listing meals for each day and noting the ingredients needed. This practice helps you stick to your budget by preventing impulse purchases and reducing food waste. Involve your family in the planning process to consider everyone's preferences and encourage participation. Working together strengthens your family unit and makes meal planning more enjoyable and efficient.

Learn More:

For help and guidance on family menu prepping, see Meal Planning: Benefits and How-To's of Family Dinners.

Fresh vs. Processed: A Savvy Shopper’s Guide

Here is a practical comparison to highlight the savings you can achieve by choosing fresh ingredients:

- A fresh whole chicken costs £5, while a pre-cooked version jumps to £8. A takeaway chicken meal? A hefty £15

- Fresh potatoes for £1 are a bargain compared to £2 for frozen chips and £3 for takeaway chips

- A fresh head of lettuce costs £1, compared to £1.50 for a bagged salad and £4 as a restaurant side

- Making a lasagne from scratch costs £6, whereas a ready meal lasagne sets you back £8. A takeaway version? £20

According to Unidine, “focusing on fresh ingredients not only promotes improved health, but also boosts nutrients and flavor profiles. Any type of processing such as canning, freezing or drying can deteriorate the quality of nutrients, fiber, flavor, and even natural color.” Adding: “It is about knowing what you’re buying.”

If you are preparing a meal with vegetables, slice enough for several meals at once. Bag and refrigerate them or freeze after blanching for 2-3 minutes. This not only stretches your grocery budget but also conserves energy. It's a method I swear by to keep my kitchen running efficiently. Got a savvy tip for me? Share it in the comments.

As we have seen, making small, informed choices in your kitchen, you can reap significant savings. By choosing fresh, planning, and prepping smartly, you turn the heart of your home into a hub of both culinary creativity and cost-efficiency. With these savings, you can dive into your next meal with confidence, knowing you are getting the best value for your money.

Emphasising fresh over processed is not just healthier—it is also more economical. Take a £3 home-cooked meal. I am living proof that it nourishes the body and the wallet, proving that culinary creativity can be a powerful ally in monetary management. Let us explore one such £3.00 example, which is my home-spun recipe I promised you at the outset.

Variety is the Spice of Life

Cooking, like any science, thrives on experimentation, like the accidental discovery of Richard T. James helical spring Slinky in the early 1940s. Did you own one? I did. These culinary adventures, from the boarding school supper nights to experimenting with budget-friendly recipes like my much-acclaimed sausage stir-fry, embody the joy of blending different ingredients and techniques.

Instead of printing it here, I have gone one step better. I have turned this special recipe into a single-page PDF document for you to download here and use at your leisure and share with your family and friends. Let me tell you, this favourite recipe of mine combines cost-efficiency and culinary creativity and is yours to keep. I would love to know what you think once you have had a chance to try it out. Furthermore, it is such a simple and inexpensive idea, you can use it as the basis for other tasty dishes just by changing the sausage for a fillet of salmon or chicken. What is more, it is very energy efficient at 0.27p at today’s prices. It would cost you more than that in fuel to pick up a takeaway in a basic family car.

Just as selecting fresh ingredients over processed ones provides tangible financial benefits, making informed decisions about household energy consumption can yield substantial savings. For me, this principle came into sharp focus during the monetary crisis of winter 2022 and early 2023, when the surge in oil and gas prices forced me to reassess how I managed my utility costs. In the following section, I will show you how I managed to shave £600 off my combined energy costs.

Mastering Utility Costs During the Financial Crisis

Those who pay their bills on time is soon forgotten.

It is only by not paying one's bills that one can hope to live in the memory of the commercial classes. -

Oscar Wilde

It was the monetary crisis in the winter of 2022 and early 2023 that prompted me to closely monitor my household energy consumption. Not that I wasn't cost-conscious before. On the contrary. With the war in Ukraine intensifying and oil and gas prices skyrocketing, I became acutely aware of the impact on my utility bills. I was not prepared to line the pockets of the fat cats any more than was strictly necessary. Although it still puzzles me why Britain’s gas prices soared so dramatically, considering only 3% of our gas came from Russia according to

Boiler Central, the substantial increases in energy costs pushed me to devise a strategy to manage and reduce my consumption effectively.

Actionable Tip:

Start by conducting an energy audit to identify high-consumption appliances and heating costs. Knowing the hourly rate for running your central heating boiler means you can budget correctly and use it confidently, keeping warm without the fear of overspending and unexpected high bills. Similarly, knowing the running costs of your gas or electric hob ensures you can cook meals without worrying about exceeding your budget. Understanding these costs allows for effective money management and peace of mind. Let me show you what I did.

Data Energy Usage Chart

I began by devising a daily energy usage chart based on the kilowatt-hour price at that time. This involved understanding the science of convection conservation—a technique to achieve maximum heat retention with minimal energy consumption. I learned how to maintain a consistent temperature even after I had turned off the heating, by keeping doors and windows closed but ventilated to optimise heat distribution throughout the home. This approach allowed me to reduce my winter daily usage to between £4-£6: £6 on particularly freezing days and £4 on milder days, which included the cost of heating, hot water, and using the gas hob.

Efficient Heating Schedules

My gas combination Worcester boiler, for example, ran at about 60p per hour. To manage my energy use efficiently, I programmed the heating to come on about 30 minutes before waking up and run for a maximum of 3-4 hours before switching off for a similar period, and then repeating the cycle. This approach kept my cold spell usage low and consistent, making me one of British Gas's most economical customers in that winter of discontent. While there were those who faced increases of 30-50% or more in their monthly direct debits, my combined fuel costs (electricity and gas) remained under £1,560 a year.

British Gas even informed me that I was so efficient that they would reduce my monthly electricity direct debit by £15. At that point, my daily usage averaged between £1.85-£2.50. Instead of spending this saving, I prudently saved it in case energy prices rose again. Similarly, when the government provided £60 a month during the crisis, I set aside these funds in my expenses account. This foresight allowed me to use the saved money to settle any excess energy costs at the end of the crisis, leaving me debt-free and stress-free.

Annual Savings

By paying close attention to my energy usage and adopting efficient practices, I not only managed to keep my utility costs low during a challenging financial period but also built a buffer against future uncertainties. My combined efforts in energy efficiency led to annual savings of approximately £600. I provide a comprehensive breakdown of my energy savings in the next but one section.

Learn More:

To better understand and manage your energy costs, check out this Understanding Your Electricity Bill Infographic by National Grid. This resource provides a clear visual representation of where your energy is going and how you can make adjustments to save money.

To reiterate, my efforts to master utility costs during the financial crisis of 2022-2023 focused on three key strategies. First, creating a daily energy usage chart helped me monitor and manage consumption, ensuring that my heating and hot water use was both efficient and cost-effective. Second, implementing efficient heating schedules, such as programming my boiler to run only when necessary, kept my winter utility bills low. Third, these combined practices resulted in annual savings of approximately £600, providing a financial buffer against future uncertainties. These steps underscore the importance of mindful energy management in achieving financial stability.

With my energy-saving strategies successfully in place, I turned my attention to another critical area: my aging household appliances. After a narrow escape with my old washing machine, it became clear that upgrading these outdated appliances was essential for enhancing efficiency and securing significant savings.

Appliance Upgrade: The Impact of Modern Efficiency

Efficiency is doing things right; effectiveness is doing the right things. - Peter Drucker

In 2022, I upgraded three household appliances: my washing machine, dishwasher, and vacuum cleaner. This move aimed to boost energy efficiency and cut utility costs, with the washing machine upgrade making the most noticeable difference.

The Old Washing Machine's Demise

My old washing machine, an 18-year-old relic, had become increasingly costly to run. Its dramatic failure occurred when the concrete block inside, meant to balance the motor, came loose. The spin cycle, reminiscent of a stampede of elephants, culminated in the door bursting open one day while I was trying to steady it. Fortunately, the water had already drained, avoiding a flood. I had to switch off the mains to stop the machine, finally putting it out of its misery.

Benefits of the New Machine

The new washing machine is significantly more energy-efficient, reducing running costs by 60%. The cost per cycle dropped from 70p to just 28p. With a 10lb drum capacity, it efficiently manages my laundry needs, including clothes, towels, bedding, and table linen. I live alone with ample clothing, so I wash no more than once a fortnight, spread over 3-4 loads. This balance ensures optimal machine performance, avoiding the pitfalls of over or under-filling.

Why Balance Matters

I have learned that overloading a washing machine restricts clothes' movement, hindering proper cleaning and stressing the motor and tub bearings, potentially leading to damage and financial hardship. Conversely, underfilling can cause imbalance as clothes accumulate on one side of the drum, leading to uneven wear on both the machine and garments. Overfilled loads cause excessive friction, wearing clothes faster, while underfilled loads subject garments to more stress, shortening their lifespan. Understanding this helps me manage costs and maintain efficient usage.

Nothing compares to the smell of clean linen fresh out of the machine. Takes me back to my childhood and my early days at boarding school, when I would stand by my bed in my dorm, removing garments one at a time from my neatly packed suitcase and holding them up close to my nostrils—relishing their every scent. It was my one link to home and my dear mama fifty-seven miles away.

By switching to a more energy-efficient washing machine, I reduced my annual energy costs from £70.76 to £28, resulting in a total annual saving of £30.24.

Dishwasher Upgrade

Similarly, my new dishwasher has yielded significant savings. This modern, energy-efficient 1.2 kWh dishwasher typically costs around thirty-five pence per cycle based on an electricity unit cost of about twenty-nine pence per kWh, making it quite cost-effective over manual washing, especially when full loads are washed. Compared to 70p per cycle for the old appliance, this latest addition has halved my running costs. Over a year, at one cycle per week, the total energy cost now sits at £18.20 instead of £36.40, representing a significant reduction in my annual energy expenses.

The New Vacuum Cleaner: A Cost-Efficient Upgrade

Upgrading my 30-year-old vacuum cleaner to the latest Kirby model brought significant improvements. Although Kirby vacuums have a higher initial cost, their exceptional performance and versatility ensure substantial long-term savings.

Why Kirby?

The Kirby vacuum excels in multiple areas, eliminating the need for separate tools or external cleaning services:

- Deep cleaning for carpets and effective performance on hard floors.

- Cleans sofas, curtains, and mattresses.

- Efficiently manages pet hair.

- Durability: The Kirby can last up to 30 years, offering reliable performance over decades, unlike most vacuums that may need replacing every five years.

Cost Savings from Kirby's Versatility

Here is how the Kirby vacuum saves costs compared to external services:

Trading my 30-year-old model in for the latest version gave me £500—bringing the cost of the upgrade down to £1,800, reaffirming that Upcycling is worth it.

Carpet Shampooing per room: External Service: £50-£60.

Kirby: £0.00.

My Saving: £200-£240 per year.

Curtain Cleaning per set: External Service: £8.

Kirby: £0.00.

My Saving: £32.00 per year.

Mattress Cleaning: External Service: £20-£35.

Kirby: £0.00.

My Saving: Between £40.00-£70.00 per year for two cleans.

Total Annual Savings: ££272.00-£327.00.

To recap: upgrading my household appliances in 2022 significantly improved efficiency and reduced costs. First, replacing the old washing machine with a new energy-efficient model decreased running costs by 60%, dropping the cost per cycle from 70p to just 28p, resulting in annual savings of £30.24. Second, upgrading the dishwasher halved the cost per cycle, saving £18.20 annually. Finally, investing in a versatile and durable Kirby vacuum cleaner eliminated the need for external cleaning services, providing annual savings of approximately £272-£327. These upgrades not only enhanced efficiency but also reinforced the importance of investing in quality appliances for financial stability.

Summary of Annual Energy Savings

In making the transition to a more energy-efficient home, here are some of the ways I have managed to cut costs:

- Turning off all electrical equipment after use saved me an impressive £315 over the year, which translates to £26.25 per month.

- Through strategic management of my heating—like using convection conservation to keep temperatures steady—I cut £150 from my annual heating costs,, ensuring my home stayed comfortably warm during winter.

- Likewise, replacing my old washing machine with a more energy-efficient model reduced my yearly expenses by £30.24.

- Similarly, upgrading to a more energy-efficient dishwasher brought my annual costs down by £18.20.

- No different when I Traded my electric oven for a slow cooker, ended up saving me a staggering £79.92 over 12 months. One of the best moves I had ever made in the kitchen. There is nothing to compare to slow cooked food.

- Lighting is a different kettle of fish. While I use lights infrequently due to sight loss—for security—the switch to energy-efficient bulbs has contributed to my overall savings. The last set of energy savers I bought boasted a longevity of 12,000 executions. Sorry to say, I have not kept a record.

- By using a thermos flask to reduce how often I need to boil the kettle, I managed to save £7.30 a year.

Useful Resources

For further insights into managing your energy costs and improving efficiency, explore these resources:

Ofgem’s Guide to Understanding Your Electricity and Gas Bills:

This guide explains the various components of your energy bill, including standing charges, unit rates, and taxes. It helps you understand where your money goes and how you might reduce costs.

Energy Cost Breakdown Infographic by National Grid ESO:

This infographic provides a detailed breakdown of home energy costs and offers practical tips on how to reduce your consumption and save money.

Citizens Advice’s Guide to Energy Saving:

This guide offers practical advice on how to save energy in your home, covering everything from insulation to energy-efficient appliances.

In Summary

To achieve a more energy-efficient home and substantial cost reductions, I took several key actions emphasizing personal responsibility and annual savings:

- By turning off all electrical equipment after use, I saved £315 over the year.

- Strategic management of my household temperature, including using convection conservation, cut £150 from my annual heating costs.

- Replacing my old washing machine with a more efficient model reduced yearly expenses by £30.24.

- Upgrading to a more energy-efficient dishwasher saved an additional £18.20 annually.

- Switching from an electric oven to a slow cooker resulted in a significant saving of £79.92 over 12 months, highlighting the benefits of slow-cooked meals.

- Transitioning to energy-efficient bulbs contributed to overall savings, with the last set boasting a longevity of 12,000 executions.

- Using a thermos flask to reduce kettle usage saved £7.30 a year.

These measures demonstrate that by taking personal responsibility and making thoughtful adjustments, significant financial benefits can be unlocked, going beyond mere cost-cutting to achieve substantial annual savings.

Imagine what these kinds of savings could mean for you. By making similar adjustments, you too could unlock significant financial benefits that go beyond just cutting costs. Let us see, shall we.

Unlocking Hidden Wealth

Beware of little expenses - a small leak will sink a great ship. - Benjamin Franklin

Just as rethinking my own money unleashed a wealth of opportunities, it could do the same for you. In my case, you may remember how it enabled me to conduct essential maintenance on my property, improve my health through quitting smoking and taking up walking, and enjoy special treats and outings without financial strain. Likewise, you could find This newfound financial flexibility useful in matters of:

- Establishing a financial safety net for unexpected expenses, providing peace of mind and financial security.

- Save for courses or certifications that can enhance your skills and career prospects.

- Budget for short holidays, weekend breaks, or even occasional meals out to reward yourself and your family for sticking to your financial plan.

Yet, to unlock hidden wealth, the first step is personal honesty and acknowledging our situations.

Personal Honesty and Acknowledging Situations

Achieving financial stability begins with an honest assessment of your situation. Recognising and addressing my financial instability was crucial for me. Similarly, in the needs and wants section, Ruth confessed her unnecessary spending and her journey towards financial discipline. She realised that buying things to cheer herself up was a hard habit to break. By sharing her story, she acknowledged the difficulty of distinguishing between needs and wants. This requires honesty about our spending habits and the discipline to address them.

Discipline and Realities of Personal Spending

Discipline is essential in personal spending, involving saying "no" to non-essentials, which can lead to significant savings. For example, my decision to quit smoking saved me £3,000 a year. Similarly, Ruth's journey towards financial discipline through personal challenges, like a 30-day no chocolate challenge, saved her £50.00 a month. She is now exploring alternative ways to boost her mood without spending money. Her story highlights the raw realities of making tough financial choices. Despite the pressure, she successfully completed a 30-day no chocolate challenge which ended up saving her £50 and is now applying the same discipline to unnecessary spending.

Recognising the difference between needs and wants isn't just about knowledge; it's about putting that understanding into practice in daily financial decisions.

Needs and Wants Transcend Beyond Knowing the Difference

Realising that smoking was a want, not a need, helped me redirect funds towards more important expenses. Similarly, Ruth's 30-day no chocolate challenge was a turning point. By recognising and acting on these distinctions, we can make more informed and beneficial financial decisions. Real-life experiences can also shed light on effective financial strategies. Consider Ruth and her journey towards better financial management.

Ruth's experience underscores the importance of setting personal challenges and finding alternatives to spending money. Her journey demonstrates the power of self-awareness and disciplined action in overcoming unnecessary spending habits. She writes: “The really great thing, aside from the money is, I've not wanted to go back to my old ways.”

Personal Strategies for Financial Management

My strategies included quitting smoking, cutting out coffee shop visits, switching to dawn walks, and adopting energy-efficient practices. These changes not only saved money but also improved my physical and mental health. Ruth found success in setting personal challenges, like her 30-day no chocolate challenge, and is now finding alternative ways to boost her mood without reckless spending. She shared: “I still have treats, but in moderation.” These small but significant steps helped her break the cycle.

Though our strategies differ, they share the common goal of improving financial health. By making conscious choices and sticking to our plans, we achieved greater control over our finances. Proof that these strategies work reinforces their importance and motivates continued effort.

Personal Testimonies as Proof of Strategy Success

My journey towards financial stability and well-being is a testament to disciplined spending and energy-efficient practices. The financial flexibility I gained allowed me to conduct essential home maintenance, enjoy special treats, and reduce stress. Ruth’s story further illustrates the success of these strategies.

In response to my Facebook post about understanding the differences between needs and wants, Ruth shared her confession of unnecessary spending. I advised her to find alternative ways to boost her mood without spending money, such as walks in the park or quality time with loved ones. Ruth’s positive response and determination to implement these changes highlight the power of community and shared experiences. She is now overcoming her habit of unnecessary spending by setting personal challenges and seeking non-spending ways to cheer herself up.

Her story exemplifies how personal honesty, discipline, and strategic planning can lead to financial freedom. By following these principles, Ruth and I have both achieved greater control over our finances and improved our overall well-being.

Our experiences highlight the importance of honesty, discipline, and strategic planning—principles crucial for unlocking hidden wealth and achieving financial stability. It starts with understanding your needs and wants, setting realistic goals, and making disciplined choices. With patience and persistence, you can transform your financial situation and enjoy the benefits of a well-managed budget.

To encapsulate, personal responsibility and disciplined spending are key to unlocking hidden wealth and achieving financial stability. Establishing a financial safety net and differentiating between needs and wants can lead to significant savings. For instance, turning off all electrical equipment after use saved £315 annually, and managing heating costs strategically cut £150 from my annual expenses. By quitting smoking, I saved £3,000 a year, which I redirected towards essential expenses and savings. Similarly, Ruth's journey towards financial discipline through personal challenges, like a 30-day no chocolate challenge, saved her £50.00 a month, highlighting the impact of making informed financial decisions. These examples demonstrate that personal responsibility and disciplined spending can transform financial situations, proving that effort truly does pay off.

From my own experience, maintaining accurate household accounts has been invaluable. It has empowered me to make informed choices, ensuring that every penny works towards achieving my financial goals. Let us explore how you can adopt these practices to gain similar control and confidence over your finances. Here are eight key steps in household budgeting that can empower your finances with a free gift included.

Empower Your Finances: 8 Key Steps in Household Budgeting

A budget tells us what we can't afford, but it doesn't keep us from buying it. - William Feather

This quote underscores the importance of not just having a budget but also exercising the discipline to adhere to it. A budget can highlight our financial limits, but without a clear understanding of income and expenses and the willpower to stick to those limits, making informed decisions becomes challenging. This can lead to unnecessary stress and potential debt. Let us explore the essential aspects of money management, with practical examples and explanations, to ensure that our financial plans are both realistic and effective.

Why It Matters

Effective money management is not just about keeping track of numbers; it is about creating a framework that supports confident decision-making and financial well-being. Accurate accounts empower you to live within your means, plan, and oversee unexpected expenses without resorting to debt. For low-income families, these practices are crucial for maintaining financial stability and achieving long-term security.

Track Every Penny

Sarah, a single mother, found herself consistently short of money by the end of the month. By meticulously recording every expense, no matter how small, she discovered that daily coffee purchases and spontaneous shopping were eating into her budget.

Tracking every penny involves documenting all income and expenses, including small purchases that often go unnoticed. This practice helps identify unnecessary spending, allowing you to redirect funds to essential needs or savings. Use a notebook, spreadsheet, or budgeting app to keep an accurate record. Regular tracking enables you to spot patterns and adjust spending habits effectively.

Create a Realistic Budget

The Johnson family set up a budget that included all their fixed and variable expenses. By comparing their budget to actual spending each month, they could see where they were overspending and where they had room to save.